In our rapidly evolving digital landscape, blockchain technology has emerged as a revolutionary force, capturing the attention of industries and individuals alike. Its potential to redefine how we conduct transactions, store data, and build trust in our digital interactions is nothing short of remarkable. As we dive into the world of blockchain, we’ll uncover its essential components, how it functions, and the myriad applications that make it a cornerstone of innovation today. Understanding blockchain technology basics is not just for tech enthusiasts; it’s crucial for anyone looking to navigate the future of digital interactions and secure their place in this new era.

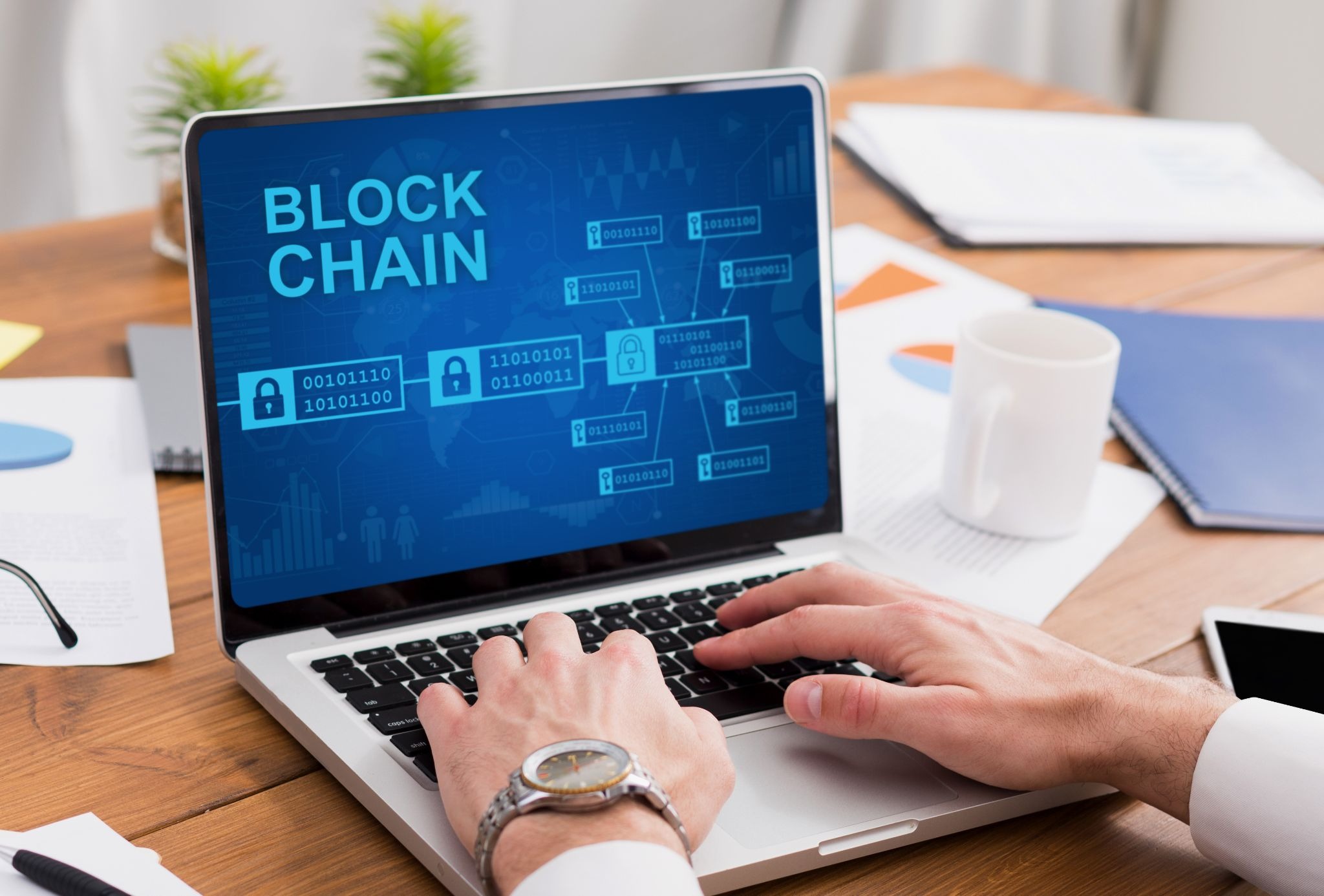

At its core, blockchain technology is a decentralized digital ledger that records transactions across multiple computers. This decentralized nature means that no single entity controls the entire chain, promoting transparency and security. Each transaction is grouped into a block, which is then linked to the previous block, forming a chain of blocks—hence the name “blockchain.” This structure ensures that once a block is added to the chain, it cannot be altered without altering all subsequent blocks, making fraud nearly impossible.

Key concepts that define blockchain include decentralization, which removes the need for intermediaries; immutability, which ensures data integrity; and transparency, which allows all participants in the network to see the same information. These features collectively enhance trust among participants, making blockchain a game-changer in various sectors.

The story of blockchain began with the introduction of Bitcoin in 2009. Created by an anonymous person or group using the pseudonym Satoshi Nakamoto, Bitcoin was the first cryptocurrency to utilize blockchain technology. This innovative approach allowed for peer-to-peer transactions without intermediaries, sparking interest in the potential applications of blockchain beyond cryptocurrency. Over the years, numerous blockchain platforms have been developed, leading to the creation of smart contracts, decentralized applications (dApps), and various other digital currencies. Today, blockchain technology is being explored in industries such as finance, supply chain, healthcare, and more, as businesses recognize its potential to streamline operations and enhance security.

Understanding how blockchain works requires a closer look at its fundamental structure. A blockchain is composed of blocks, each containing a list of transactions. When a new transaction occurs, it is broadcast to the network, where it is verified by participants, known as nodes. Once confirmed, this transaction is added to a new block alongside other validated transactions. Each block contains a unique cryptographic hash of the previous block, creating a chain that links all blocks in chronological order.

The nodes play a crucial role in maintaining the integrity of the blockchain. They validate transactions based on predetermined consensus mechanisms, ensuring that all participants agree on the state of the ledger. This decentralized verification process eliminates the need for a central authority, fostering trust among users.

The journey of a transaction through the blockchain network involves several key steps. First, when a user initiates a transaction, it is broadcast to the network. Nodes then compete to verify the transaction through a consensus mechanism. In the case of Bitcoin, this is achieved through Proof of Work, where miners solve complex mathematical problems to validate transactions and add new blocks to the chain. Once a block is successfully mined, it is added to the blockchain, and the transaction is considered confirmed.

In contrast, other blockchain networks may utilize different consensus mechanisms, such as Proof of Stake, which relies on validators holding a stake in the network. Each mechanism has its strengths and weaknesses, influencing transaction speed, energy consumption, and security. Understanding these processes is essential for grasping how blockchain technology operates and its implications for various industries.

Not all blockchains are created equal; they can be classified into public and private networks, each serving different purposes. Public blockchains, like Bitcoin and Ethereum, are open to anyone. They allow users to participate in the network, validate transactions, and view the entire transaction history. This openness fosters transparency and inclusivity but can also lead to scalability challenges due to the high number of participants.

Blockchain networks can also be categorized based on access control. Permissioned blockchains require users to obtain permission to join the network and participate in transactions. These systems are often used in enterprise settings where data privacy and regulatory compliance are paramount. They can enhance security and streamline operations by restricting access to trusted participants.

Conversely, permissionless blockchains grant open access to anyone, allowing users to join freely and participate in the network without authorization. This model promotes decentralization and democratizes access to blockchain technology, encouraging innovation and collaboration among users. Each type of blockchain network has its unique advantages, catering to different needs and use cases.

Blockchain technology has made significant inroads into the financial services sector, revolutionizing how we conduct transactions. Cryptocurrencies, the most well-known application of blockchain, enable peer-to-peer transactions without the need for intermediaries like banks. This has led to lower transaction fees, faster processing times, and increased financial inclusion for unbanked populations.

Another area where blockchain technology shines is in supply chain management. Traditional supply chains often face challenges related to transparency, traceability, and accountability. Blockchain provides a solution by allowing all participants in the supply chain to access a single, immutable ledger that records every transaction from production to delivery.

With blockchain, companies can track the origin of products, monitor their journey, and verify their authenticity. This transparency not only helps reduce fraud but also enhances consumer trust. For instance, in the food industry, blockchain can trace the journey of a product from farm to table, ensuring that consumers know where their food comes from and how it was handled. As businesses recognize the power of blockchain to improve supply chain efficiency, its adoption is expected to grow.

Despite its numerous advantages, blockchain technology faces significant challenges, particularly regarding scalability. As more users join the network and transaction volumes increase, many blockchain systems struggle to process transactions quickly and efficiently. For instance, Bitcoin can handle only a limited number of transactions per second compared to traditional payment networks like Visa.

Various solutions are being explored to address scalability issues, including layer 2 solutions like the Lightning Network for Bitcoin and sharding techniques for Ethereum. These innovations aim to enhance transaction throughput while maintaining the security and decentralization that blockchain technology is known for. Understanding these challenges is crucial for stakeholders looking to implement blockchain solutions effectively.

As blockchain technology continues to gain traction, regulatory and security concerns remain prominent. Governments worldwide are grappling with how to regulate cryptocurrencies and blockchain applications, often struggling to keep pace with the rapid evolution of technology. Unclear regulations can hinder innovation and create uncertainty for businesses looking to adopt blockchain solutions.

The future of blockchain technology is promising, with emerging trends poised to reshape its landscape. One notable trend is the increasing focus on interoperability—the ability of different blockchain networks to communicate and share data seamlessly. As the number of blockchain platforms grows, ensuring they can work together will be crucial for unlocking their full potential.

As we look ahead, blockchain technology holds the potential to facilitate a more decentralized and equitable digital ecosystem. By removing intermediaries and enabling peer-to-peer interactions, blockchain empowers individuals and communities, fostering a sense of ownership and control over their data and transactions. This shift toward decentralization can lead to new business models, enhanced privacy, and increased trust among users.

What is blockchain technology?

Blockchain technology is a decentralized digital ledger that records transactions across multiple computers, ensuring transparency and security.

How does blockchain work?

Blockchain works by grouping transactions into blocks that are linked together in chronological order. Each block is verified by network participants, ensuring data integrity.

What are the types of blockchain networks?

There are public and private blockchains, as well as permissioned and permissionless networks, each serving different purposes and use cases.

Category :